{kind=link}

[ad_1]

krfetch/E+ via Getty Images

investment thesis

Melco Crown Entertainment Limited (Nasdaq:MLCO) is a company that develops and manages resorts. The company operates casinos in Macau and the Philippines.The company’s share price has grown strongly in the last year At about 127%, the shareholder return is strong.I attribute these good results to Ease of Covid 19 restrictions This boosts gambling and the growing casino market.

Despite these solid results, I’m skeptical about the company’s future given its debt load and looming recession. I think these two aspects mask the optimism of the growing casino market.

Quite a lucrative year for investors

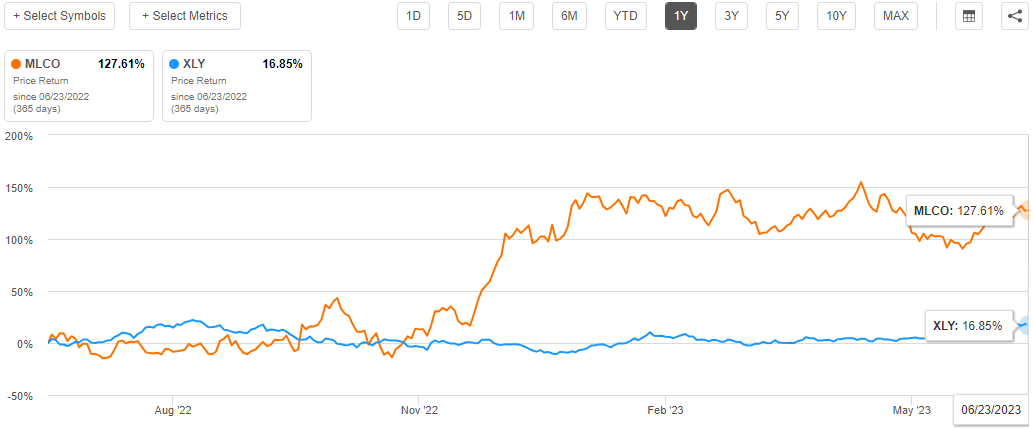

Buying an index fund is simple these days and your returns should roughly track the market. However, investors can increase returns by investing in companies that outperform the market. MLCO stock price rose 127.61% from pre-listing A year ago, it outperformed the market median by about 16.85%. If it can sustain its outperformance over the long term, investors will do very well! Long-term returns, on the other hand, are negative, as shares are down about 54% from five years ago, raising concerns about the long-term sustainability of last year’s solid returns.

looking for alpha

Let’s examine the company’s long-term fundamentals to see if they line up with the results investors are seeing. Since the company hasn’t turned a profit over the past year, I’ll check its revenue expansion to get an idea of its health. A company that has been losing money for years should quickly increase sales. If sales continue to grow rapidly, this usually leads to a correspondingly rapid increase in profits.

Compared to the previous year, MLCO’s revenue was Down 19.15%. Shares have soared about 127% during that time, despite lower sales. Rising stock prices do not correspond to growth in company revenue or profits, but the market appears to have priced in weaker results; therefore, investor sentiment may rise.

Happily, MLCO shareholders achieved a total shareholder return of approximately 127% over the past year. While the long-term decline makes me wary, the recent uptick in total shareholder return points to a brighter future. While market conditions are important in their impact on stock prices, there are other factors to consider, some of which I will cover in my analysis.

A Growing Market: A Potential Sales Catalyst

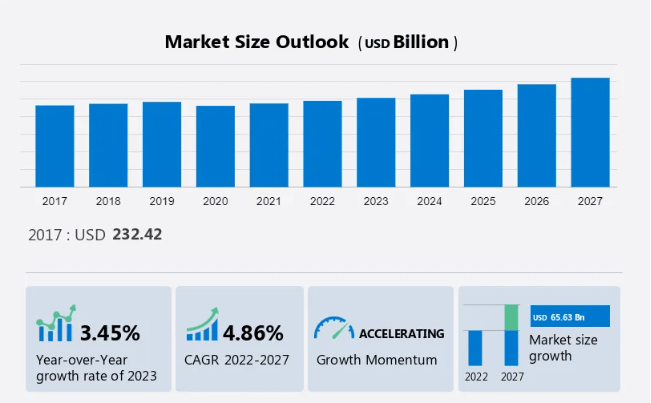

compound year growth rate The casino gaming industry is expected to grow by 4.86% between 2022 and 2027. The market is expected to grow by $65.63 billion. Several reasons, including increasing disposable income of consumers, widespread adoption of internet casinos, and general rise in gambling interest, will aid in the expansion of the market.

technology navigation

The casino gaming industry is growing due to the spending power of customers. The rise in dual-income households explains the world’s high per capita disposable income. This makes high-end services such as casino games cheaper, boosting purchasing power in developed countries. The number of working women has also increased worldwide. Higher incomes will allow people to spend more on sports betting and other leisure activities. High earners use it as a status symbol.

Due to the expansion of game types in recent years, the demand for casino games is on the rise. Online casino games are despised for being cheap, obscure and risky. However, the market is expected to experience considerable expansion over the forecast period owing to rising revenue levels and increasing investments by providers in online platform security.

An important factor affecting the expansion of the casino gaming industry is the increasing use of social media marketing. Online and offline casinos utilize social media marketing techniques to attract customers. Social media sites such as Facebook, Instagram, and Twitter are growing globally due to the proliferation of smartphones and better internet connections. Providers use cutting-edge marketing techniques to promote gaming events and casinos, as they recognize the reach of these social media platforms.

Given these promising market trends, I expect MLCO to increase its market share and expand its revenue base as the market grows. In my opinion, this gives us reason to hope for better revenue and ultimately profits if the company capitalizes on this growing market. I think the company is trying to adapt to the growing market by leveraging development initiatives.For example, in MRQ, they launched the second phase of Studio City, the Epic hotel building and indoor water park opened, and opened the first series of residency concerts in Macau. To round out their hotel portfolio in Macau, they also hope to open the W hotel tower in September.

debt situation

The main investment risk is not price fluctuations, but the possibility of irreversible loss of funds. Since too much debt can lead to bankruptcy, I always want to consider a company’s use of debt when assessing a company’s risk.

MLCO’s total debt is $8.2b. However, it did have $130 million in cash to offset that loss, resulting in net debt of around $680 million.According to the most Most recent balance sheet dataMLCO has short-term liabilities of $867.7 million and long-term liabilities of $7.77 billion. As compensation, it has $1.3 billion in cash and $69.7 million in accounts receivable. As a result, its liabilities exceeded total cash and receivables by $7.26 billion. The shortfall weighed heavily on the company’s $5.57 billion market cap. Ultimately, if creditors demand repayment, the company may need to undergo a substantial recapitalization, which could lead to massive dilution.

In addition to high debt, the most important thing is whether the company can repay the debt. To determine these, we look at the company’s EBIT coverage ratio and available cash flow on a TTM basis. MLCO’s EBIT loss of $584.2 million was insufficient to cover its $398.6 million interest expense. Also, cash flow is an important aspect of debt repayment since accounting profit cannot be excluded from debt repayment. As if the lack of interest coverage wasn’t enough, the company has a leveraged free cash flow balance of -871.11 million.

From these figures, the company is clearly a risky investment because in addition to its high debt, the company is insolvent and therefore has a high risk of default.

looming recession

economic experts are become less and less optimistic The much-discussed recession of 2023 will actually happen. Economists at Wells Fargo were the latest experts to cut their recession forecasts for this year. The recession will begin in early 2024, the company said.

Talk of a recession awaits as people wait to see how the economy will respond to the Federal Reserve’s most aggressive rate hikes in 40 years. A “soft landing” (meaning the U.S. economy slows only slightly) or a “hard landing” (meaning the Fed causes a deep recession and high unemployment) are two possible ways the economy can recover from rate hikes.

The Nasdaq is up nearly 26% this year, while the S&P 500 is nearly in the midst of a bull market. The stock market is considered a forward-looking indicator. Therefore, if a severe recession still occurs in 2023, the market will not take this scenario into account. That means investors should brace for losses if that happens, as recent prices don’t seem to be pricing in a possible recession in 2023.

For MLCO, the possibility of a recession, either starting this year or early next year, is out of the question. This is due to the company’s continued struggles with profitability and imminent bankruptcy due to its large debt load and weak financial foundation to service debt.

my final thoughts

While I see some optimism in the growing industry, I think that optimism is being overshadowed by a looming recession, which will exacerbate the company’s high debt load and poor profitability when I say the company’s financial crisis. From where I stand, I rate the company a Hold until economic uncertainty subsides and its financial fundamentals improve. For more cautious investors, I think now may be the time to get out early before more crises emerge.

[ad_2]

Source link