{kind=link}

[ad_1]

Paddington

” It was one of those ecstatically chaotic times in finance, when for a brief moment anything seemed possible, the miracle became mundane, the outcast was abandoned, the feeble walked…” Author of The Predator’s Ball Connie Bruck.

It has been nearly five years since the US Supreme Court overturned the PASPA law and kickstarted the explosion of legal sports betting in the US. The next five years were like the Yukon Gold Rush in the 1840s. Just like that time period, it is packed with adventurers from all over the world. They’re all still racing to lure customers with overheated promotional giveaways. But to the delight of investors, the pace of marketing spending is starting to slow, which bodes well for the industry as a whole going forward. Time to go long with our top picks in the sector:

Flutter Entertainment (OTCPK: PDYPY), traded over-the-counter in the United States.

Many investors’ get-rich-quick dreams were dashed after hearing some analysts predict the market would hit $200b by 2025. Some people who bought in early and got out did well. Other true believers persisted and were killed. DraftKings, Inc. (DKNG) shares soared to $72 in 2021 and have since fallen below $14.

Some true believers held on but lightened their positions. Among them, Cathie Woods’ Ark Investment Management ranked second among institutional holders of DKNG with 24.7 million shares worth US$322 million after selling 368,418 shares in 3Q22. The other largest holders are Vanguard and Black Rock, both of which have positions in DKNG at the time of writing.

We cite DKNG because it is a pure space game between the leaders and not a unit of a parent casino like BetMGM (MGM) or Caesars Sportsbook (Czech Republic) – are top operators.

The inevitable shake-up has now sent the industry into the second phase of the year, where the sheep and goats will separate and frantic promotional spending will drop. The battle for market share in both new and mature markets has evolved into four leaders controlling approximately 65% of total revenue each month, with others vying for the remaining share.

Google

Above: Long distance, all arrows pointing north for Flutter.

The largest kahunas in the country to date include New York, New Jersey and Pennsylvania. (Despite an insane 51 percent tax rate on online gaming, New York state has an above-average hold rate.)

Three states have produced impressive handles since May 2018:

- Pennsylvania: $18.1b deal wins $1.4b hold 7.8%

- New Jersey: $32.6b deal wins $2.2b hold 7%.

- New York: Deal $15b, win $1.2b, hold 8.4%.

(Note: New Jersey was an early entrant into the sports betting race, which shows how time plays a role in retention. Long-reviewed statistics show sports betting has had an expected normal hold rate of 7% for decades. This is Long-term expectations are best suited for valuing stock companies in industry revenue forecasts.)

Still, the industry’s first phase (2018-present) totals have impressed investors:

Over nearly three years of operation, this is cumulative:

Total processing amount $181.4b

Total win: $13.7b.

The holding ratio is 7.6%. So you can see that all 28 states are in action, with two more opening up soon, holding percentages that are moving towards long mathematically proven advantages that were built into the odds making system decades ago.

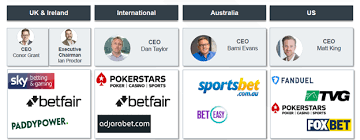

second stage: Time to pick winners and go long, sleep well and wait for solid returns ahead. We limit our best bets to Tier 1 platform stocks because they make up a disproportionate share of the overall market. It’s all about the size of the field. Tier 2 and Tier 3 sports betting stocks have a place in the industry, but the 10 companies that occupy those tiers are all single-digit market share companies and are likely to see considerable consolidation over the next five years. Bottom: Flutter’s multiple platforms include the top performing brands in the space.

Flutter Archives

Sportsbooks will certainly benefit from the 2020 pandemic as people are stuck at home. Now, as we enter the early post-pandemic era, the key for Kingdom is to make size bets as we face a possible recession.

Interloper: Investors need to be on the lookout for possible market disruptors. First, Fanatics, a privately held online marketing company for team apparel, announced that its entry into the sports betting space could come as a SPAC in the second quarter of 2023. The second, which is a really funny clown, is ESPN, and according to an as-yet-unclear assumption, Disney will at some point wake up from a long nap and post a sale sign across the network.

If that happens, expect ESPN to either buy a second-tier operator or decide to go it alone. Activist Nelson Peltz bursts into Disney (Insurance) may strengthen that prospect by pressuring Robert Iger to abandon his earlier stated hamada, hamada, hamada position (and that of interim successor Bob Chapek) and sell ESPN.

Either way, both entries may break. But they’ll all be late, as it’s more likely to buy one of the mid-cap carriers and recast it as ESPN Bets. None of these developments are likely to hurt our stock picks in the sector, as Flutter’s data is too deep, it’s too big, and it’s likely not too far away from its biggest move, spinning off FanDuel.

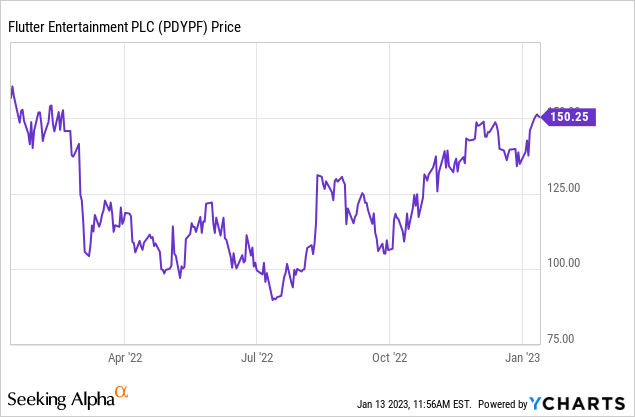

Our Picks: FLUTTER ENTERTAINMENT – Available in the US

Price to write: $150.10

52-week range: $88,30–$163,48

Market cap: $26. 4b

All-time high: 4/21 $205.11

Our PT: to 2Q23: $183.50

FWD P/E Ratio: 29.07.

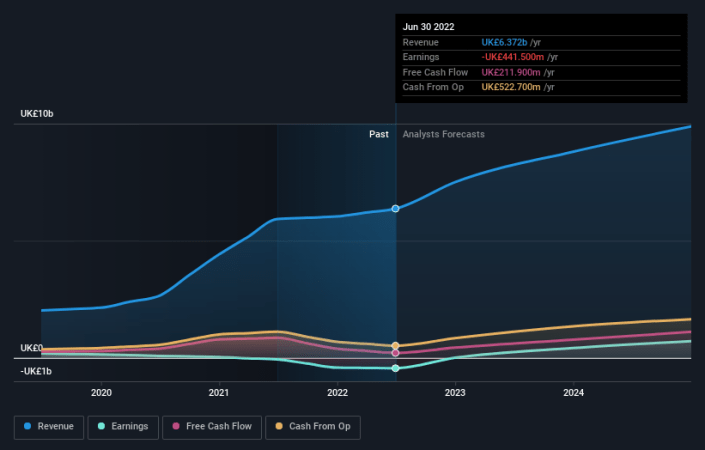

Parent company FLTR’s return over the past five years: 41%. Its revenue grew 33% annually during that period. Revenue will continue to grow strongly due to FanDuel’s strong performance in the US.

7% total shareholder return over five years

UK/Ireland-based Flutter Entertainment is by far the world’s largest online and live sports betting and iGaming platform, generating over $630 million in global revenue, with FanDuel’s US operations contributing – by company numbers – 2.9b to 3.2b Dollar 2022 revenue.

In the second quarter of 2022, FD was the first to report a quarterly profit of $22 million for the period. Its forecast for fiscal 2022 will show losses narrowing to $300 million. We’ve put the company’s 2023 forecast to our own test and believe Flutter US will show full-year overall profits in the US, while most competitors may still be before mid-2024 while reducing promotional expenses Stay a net loser.

One of the fundamental reasons to be long PDYPY stock is the inevitable spin-off of US market leader FanDuel, which by various calculations is valued at between $11b and $15b, roughly half the parent company’s current market capitalization. Another is its global power.

Market Share US

Companies’ market share requirements vary widely from state to state. Sometimes within a month we can see one platform bet more than another by mid-single digits, while the other platform does the opposite. Promotional deals come into play. Overall, FanDuel is without a doubt the leading platform in this space, with an actual market share between 37% and 42%. DraftKings came in second with a nationally adjusted range of 22% to 29%.

The next two are casino operators. BetMGM, which is 50% owned by it and British gaming giant Entain. MGM continues to emphasize its desire to acquire Entain. (We think it’s likely this year.) The fourth is Caesars Sports Book, which is very strong in Big Kahuna State. The combined market share of the two companies is about 15%. This leaves the remaining companies with single-digit shares, likely to grow with market size, but still hold relatively single-digit shares.

In Flutter, if you will, you get the “unpaid” bonus, FanDuel’s eventual spin-off, which will make it the single largest game in US sports betting, and the record holder is bound to be in the process Get a premium of one point or another. So, holding on to Flutter for the long term now should comfort holders as it provides a solid foundation for a global leader in sports betting, a dominant share leader in emerging US markets, and a parent company with a track record.

Markets to 2026

Google

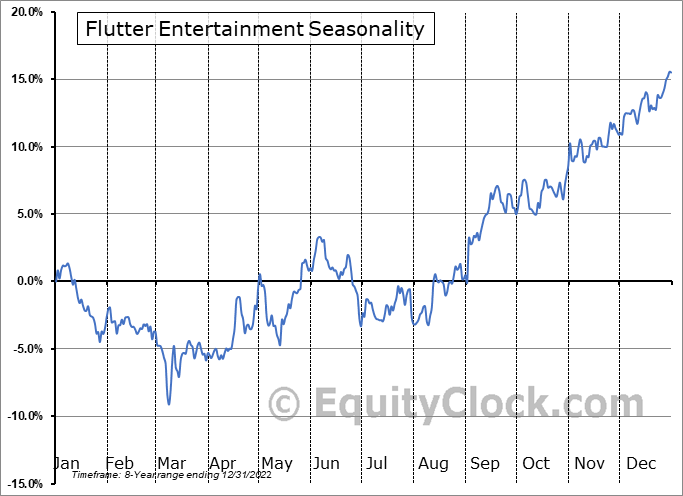

Above: FanDuel is entering its most profitable quarter of the season, largely due to increased interest in the NFL playoffs, Super Bowl and NBA.

Since legalization, we have been tirelessly monitoring the leader’s legalization pace, revenue streams, market share and platform improvements. Looking at future trends, we expect the market to be between $25b and $33b by 2025/6. JPMorgan has also come close to this assessment. One of the difficulties in looking forward to sports betting’s forward revenue projections is the ongoing unknown regarding states that are not yet legal but could be legal in 2025.

The second question is about the performance of the states that have recently joined the party: Ohio and Massachusetts, both of which are the jewels of Ohio because of its presentation and its presence in professional and college sports. It has six professional sports teams, the Ohio State University football team, and more than 40 Division I varsity teams. Fan enthusiasm is high and betting volume should follow. Massachusetts has 4 professional teams and a far less frenetic college gaming scene, although it has a large number of campuses, with fans especially enthusiastic about the Red Sox and Patriots.

Our operating assumption here is that large cities like California and Texas are completely unpredictable and cannot yet be accounted for in addressable market forecasts.

I dug into statewide demographics looking for the largest number of people with a strong generational sports betting profile and came up with an addressable market of approximately 40 million real, frequent bettors.

On this basis, I’m now increasing my original 2026 gross gaming win forecast to $50b. Assuming existing market share remains stable, i.e. up or down a few percentage points, I think a realistic forecast for 2026 FD revenue of 30% would translate into a $15b business with roughly $7.2b in gross profit.

We cannot realistically forecast EBITDA numbers as we are essentially dealing with a low margin business which depends on management skills in terms of cost efficiencies, capex needs and future technology small moats. So far, we think this is Flutter’s strong suit, as they have not only been successful in the US, but have similarly strong performances globally. Of course, the question that remains for parents is the imminent impact of new UK gambling regulations that strongly break down the number of optimal and other restrictions on betting to curb the spread of problem gambling.

in conclusion

Department leadership is always important as it largely showcases differences in management skills among peers. While all peers in long-lived industries bring good operational capabilities to their businesses, some will always be more flexible, creative, and innovative than others. We believe that at this point, on all fronts, US-listed Flutter stock (essentially FanDuel) promises to deliver the best returns to investors among all its peers. DKNG is still firmly in second place, but we need to see more cost discipline than we’ve seen so far.

That’s not the rap the other two top platforms get. But while live and primarily online sportsbooks present excellent sales growth opportunities for MGM and CZR, their bread and butter will always be the brick-and-mortar casino business. Now, with the early post-pandemic period looming and Vegas on fire every weekend, both will shine.

But in our opinion, even with its high price, Flutter Entertainment plc represents the best stock you can bet on for the next five years in sports betting.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

[ad_2]

Source link